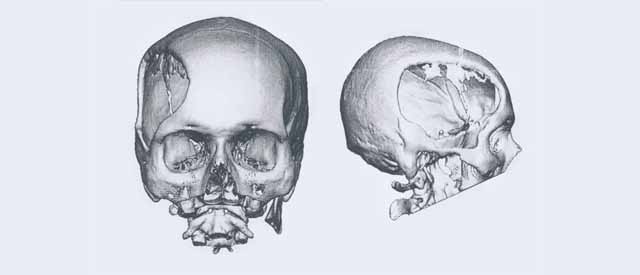

Just this year alone, three workers came to the attention of Transient Workers Count Too with holes in their skulls resulting from workplace accidents (see story here). They needed cranioplasties — reconstructing the missing part of the skull with synthetic material — but who would pay for the operation?

Their cases highlight a gap in the provision of medical care for low wage migrant workers. The Ministry of Manpower’s rules establish a ceiling for employers’ liability for medical expenses, as detailed below. This ceiling is sufficient to cover most workplace accidents, but leaves a gaping hole when the accident requires lengthy hospitalisation or multiple operations.

Explaining the rationale for setting a ceiling,

MOM’s Work Injury Compensation:

As WICA seeks to strike a fair balance between compensation for employees and the obligations placed on employers and their insurers, MOM has to set a clear limit to the compensation for medical expenses in order to provide certainty to employers. The new limits for medical expenses will continue to fully cover more than 95% of claims where hospitalization is required. The one-year cap is adequate as most injuries typically stabilise within a year from the accident. Employees who wish to claim the full medical expenses beyond the cap can choose to do so under common law. Needy cases can also apply through the hospital’s medical social worker for assistance on a case-by-case basis.

— From MOM’s FAQ webpage. Link.

Indeed, most work injury cases do not involve medical expenses that breach the ceiling. However, a small number do, and the ministry’s suggested solutions are not straightforward enough to provide an assurance of treatment. Where does that leave the injured worker?

Head injuries resulting in the removal of a portion of the skull highlight precisely this problem. Treating the initial injury is expensive enough, but what about the subsequent cranioplasty, without which the workers’ quality of life would be seriously impaired?

A condition of Work Injury Compensation Act (WICA) is that employers of migrant workers are liable to pay for medical expenses “Up to $25,000 or one year from date of accident, whichever is reached first”. The cap has been increased to $30,000 in the case of accidents occurring on or after 1 June 2012. (Source: http://www.mom.gov.sg/

A condition of Work Injury Compensation Act (WICA) is that employers of migrant workers are liable to pay for medical expenses “Up to $25,000 or one year from date of accident, whichever is reached first”. The cap has been increased to $30,000 in the case of accidents occurring on or after 1 June 2012. (Source: http://www.mom.gov.sg/

But what if medical expenses exceed these limits?

Employees would bear the excess medical expenses beyond such limits if they opt to claim for compensation under the act. Alternatively, employees can choose to seek damages at the civil courts if they wish to recover the full medical expenses, and should not file a Work Injury Compensation claim with the Ministry of Manpower (MOM).

— http://www.mom.gov.sg/

Documents/safety-health/WICA- Guide-(English).pdf

A problem with suggesting to workers that they can claim for more via the civil courts is that in practice, there are serious difficulties with this route. Firstly, workers need to prove that the injury was the fault of the employer, and this is very hard to do especially if months have passed — months the worker spent partially recovering. Secondly, there are court costs that the worker needs to pay in advance and the typical worker, already laid off as a result of the injury and without an income, will not be able to afford them. He may not even be able to get the court process rolling.

However, a separate condition of the work permit (which comes under a different law, the Employment of Foreign Manpower Act) mandates a further $15,000 of medical coverage annually, quite separate from the requirement under Work Injury Compesnation Act (WICA):

The employer shall purchase and maintain medical insurance with coverage of at least $15,000 per 12-month period of the foreign employee’s employment (or for such shorter period where the foreign employee’s period of employment is less than 12 months) for the foreign employee’s inpatient care and day surgery. . .

Taken together, this should mean that employers are required by law to purchase two separate insurance policies, and between the two of them, have insurance cover to pay up to $40,000 ($45,000 for accidents on or after 1 June 2012) in medical treatment. It is therefore hard to understand why MOM has set a lower ceiling of $25,000 (now $30,000). After all, if an employer has paid his premiums for both insurance policies – one for medical care and the other for work injury, including medical care subsequent to the injury — why does the ministry stop an employer from accessing the full amount of benefits contained within the policies?

—-

The accompanying story, Three cranioplasties, illustrate the problem discussed here through the real experiences of Majibar, Mosa and Lablu. Each of them needed additional surgery to fit a replacement piece to their skull. The cost of the surgery would push the total medical cost beyond MOM’s ceiling. Do they get the surgery, or will they have to go through life with a hole in their heads?

One of the reasons why medical expenses so quickly breach the ceiling is because all subsidies have been withdrawn for foreigners, even if they are working in Singapore and contributing to our economy. They are charged the “Others” rate, and the difference is still significant for C Class wards.

In Lablu’s and Mosa’s case, their companies paid about six times more than they would have if a Singaporean had required hospitalization and intensive care. Additional medical charges are also billed at an unsubsidised rate, which makes everything substantially more expensive.

The higher charges for foreigners is understandable for medical tourists from abroad, or emergency cases medevac’d to Singapore with hefty insurance policies. But this policy makes little sense for migrant workers brought to Singapore to meet the needs of our economy, who are paid some of the lowest salaries here, and who hold some of the most hazardous jobs.

Who is responsible for such cases when employers refuse to cover additional medical costs, and the Ministry of Manpower doesn’t insist on it? Should a medical emergency fund be available so as not to penalize small companies with medical bills beyond the capped amount?